Nobody knows what the future has in store. None of us can know what the future looks like for ourselves and our families. The only certain thing is that we’ll die at one point or the other. We don’t know how long it’ll take. It might be after 50 more years, 40 more years, or 20 more years. If you like to think that you might live a little longer than the next one decade or so, this article introduces you to the basics of Long Term Care insurance.

This page contains comprehensive info about LTC Insurance, including stats, quizzes, and handy policy details that might help your quest for the right plan. You might want to print this page for future reference. If you’ve got any question you need resolved, simply send us a quick message and we’ll contact you right back.

Why you may need to receive Long Term Care

Below are some eventual health ailments that necessitate the need for long term care:

- Parkinson’s Disease, and any Organic Brain Syndrome

- Senile Dementia, Alzheimer’s Disease

- Bone Fractures

- Arthritis

- Depression

- Diabetes

- Cancer

- Heart Disease

- TIA’s

- Strokes

Some meaningful statistics

- Nearly 50% of American citizens over 85 years old have Alzheimer’s Disease

- At age 65, the life expectancy for men is 80.2, and 84.9 for women.

- In 75% of couples, one partner (at least) will need to receive Long Term Care at one point.

Note: Crisis managing the problem after it already happens is never a good idea. This can be compared to buying auto insurance after you’ve had a car accident. As goes the old adage, ‘prevention is better than cure’.

65% of Americans think they might never need to receive nursing home care. But is this true?

Most people don’t love to toss the idea that they’ll need long term care at one point or the other, whether in the form of assisted living, community care, nursing home care, at-home care, or any other care type for that matter. That’s probably why, in the recent past, so many folks failed to plan for Long Term Care.

So what happens? When time comes and people realize that they need Long Term Care, their finances are caught off guard. The logical thing to do is ‘crisis manage’ through the situation, which usually involves seeking help from children and the immediate family. In a ripple effect, the children are also caught off-guard. They have no idea how to get Long Term Care for their parents, and they might not even know how to bankroll it.

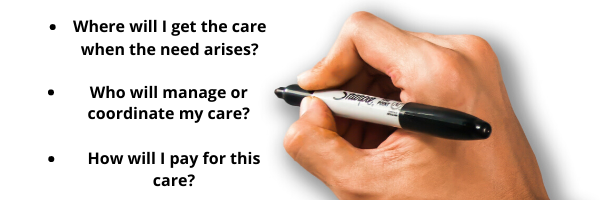

To avert this situation where your family is forced to manage a crisis, answer the questions below regarding Long Term Care.

Planning ahead is the answer to all these questions.

Could my savings cover the catastrophic cost of LTC?

You probably are already aware that Medicare pays petty little for LTC. Medicaid also pays after you’re broke and literary no money left.

The fact is that if you need LTC the money comes out of your family’s savings. However, most family’s savings cannot adequately cover a couple years of LTC costs. That’s probably why nearly three quarters of seniors in nursing homes today get support from Medicaid. For people on Medicaid, their choices are narrowly restricted to only care facilities that have optionally agreed to open up for this federal government program. That means you might not necessarily get a home that want your loved ones to stay in. So if Medicaid and Medicare won’t do it for you, what’s the answer?

LTC Insurance: What plan is adequate for your family?

Folks who are buying Long Term Care plans usually do so due to one or more of these reasons:

- They hate the idea of being a burden to their spouse, children and family.

- They are looking to arrange for top-quality LTC care for their family members and themselves.

- They are looking to preserve their own savings for a spouse, children or family.

- They want to keep their independence.

What’s affordable Long Term Care?

Long Term Care Insurance becomes affordable when you buy coverage without depleting your savings or negatively impacting your lifestyle.

What major risks are you insuring?

- Home, burglary, and fire insurance?

- Medical insurance?

- Auto damage & liability insurance?

- LTC Insurance?

Yes, all these are reasonable risks that need insurance, but chances are that you do not want to risk your savings to the biggest risk that you face during retirement. The devastating cost of LTC can involuntarily dispose your savings.

Where do you get money to clear your LTC Insurance Premiums?

LTC insurance is not a fit for everyone. But if you’ve got savings of over $105,000, you are better off subscribing. Premiums are simply a tiny fraction of the value they protect, so with smart selection of benefits you can arrive at the right measure between excess and not-enough. Keep in mind that there are many LTC Insurance riders add features you do not need, thus pushing the costs up.

The costs of Long Term Care can catastrophically wipe out your savings. It makes sense to note that your LTC insurance serves as your emergency money in retirement.

If you find that LTC Insurance cover makes sense to you, what next step you should take?

Identify a company from which to buy Long Term Care Insurance. It goes without saying that you’ll need some expert guidance to make a good decision on this one. Unlike individual financial advisors who might be well versed in one or a few LTC insurance company, our team at LTC Key knows the industry outside out. So we furnish you with highly edible insider industry knowledge that you can use to make a smart decision based on your individual circumstances and needs.

Key basics of LTC Insurance that you should keep in mind

- The company – as a general rule of the thumb, you want to settle on an LTC Insurance firm that has scored an A rating from A.M. Best. Think twice before you buy from a firm that’s just started out the other day. You want to get the assurance that your insurance company will be around to pay the claim when you need it (which might be after the next 2 or 3 decades).

- The plan – most local agents will have you choose from a list of 1 or 2 companies. But often times, this is not enough variety. So you’re better off working with a comprehensive outfit like LTC Key that makes it possible for you to shop from the entire market. This way, you end up saving both time and money. You also have more flexibility on how much coverage to purchase. We also highly advise our clients to go for plans that account for inflation!

- The price – this is another very important factor that most people think about before they buy Long Term Care insurance. When choosing from the best blue-chip carriers, go for the firm with the best price.

End-note – basics of Long Term Care Insurance

To conclude this Long Term Care basics guide, we advice that you buy the right LTC policy for you by finding that middle ground before too much and too little coverage. Keep in mind that not all firms that sell Long Term Care coverage offer quality. So you want to take time, do your homework and shop around. A good idea is to get quotes from about 3 to 5 companies. But how do you do this? Work with an LTC agent who has market-wide coverage. Study the statistics to understand how LTC coverage and claims work. This way, you should get a great deal based on your needs!